Gunpowder

Sent:9:00 PM IST{}

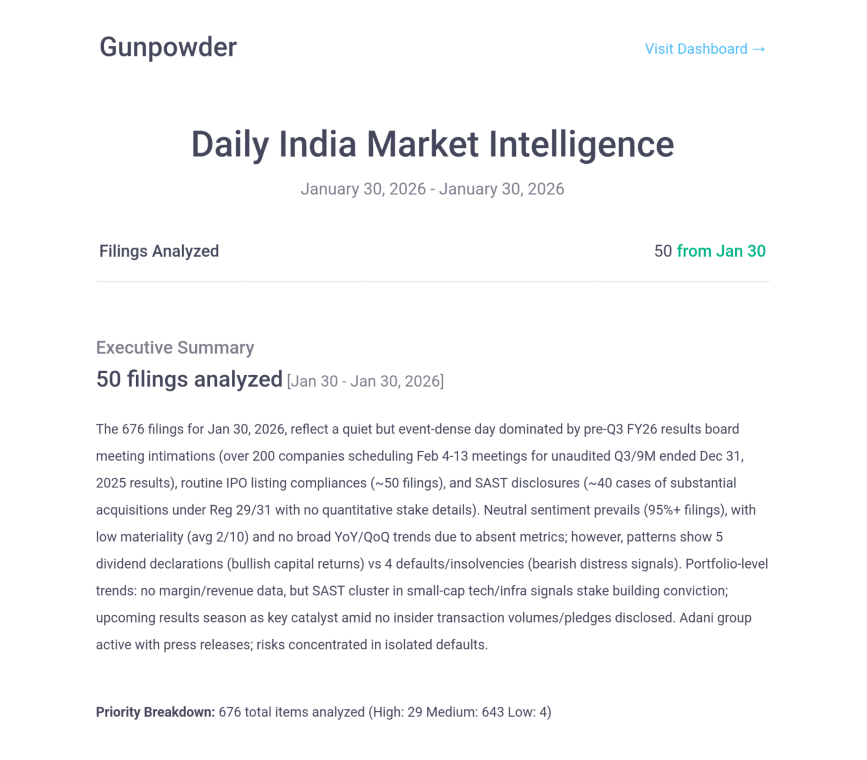

Daily India Market Intelligence

March 10, 2026

Filings Analyzed

50from Mar 10

Executive Summary

50 filings analyzedMarch 10, 2026

Across 50 filings dated March 10, 2026, dominant themes include promoter confidence via small stake buys in small-caps (e.g., Shalibhadra, Vibhor Steel, Justo Realfintech), frequent governance updates with near-unanimous shareholder approvals for director re-appointments (e.g., Laxmi Organic 99.93%, Hester Biosciences 99.54%), and multiple SAST disclosures by Shripal Shah signaling potential stake-building in financials/tech (Escorp, Aryaman entities). Period trends show mixed growth: strong in Bartronics' target (turnover +255% YoY FY24, +132% FY25), flat in Adani's DPJ TOT (+2.8% FY25), declines in AK Capital Finance (turnover -19.8% 9M FY26, PAT -26.1%), and losses in Setubandhan (FY25 net loss ₹1.51 Cr). RBI amendments clarify NBFC owned funds/Tier 1 capital computations, aiding compliance but neutral impact. Fundraising ramps up via rights issues (Tuni ₹49 Cr), capital hikes (Bajaj Hindusthan, Narmada), and investments (Avio ₹1 Cr). Infrastructure M&A positive (Adani ₹1,342 Cr EV), IPO listing (Artemis), and IP wins (Godavari patent) highlight growth catalysts, while encumbrances and sells flag caution. Overall, bullish insider conviction outweighs minor risks, with portfolio-level promoter buying trend (6+ instances) suggesting undervalued small-cap opportunities amid regulatory clarity.

Priority Breakdown: 50 filings analyzed — High: 5, Medium: 45, Low: 0

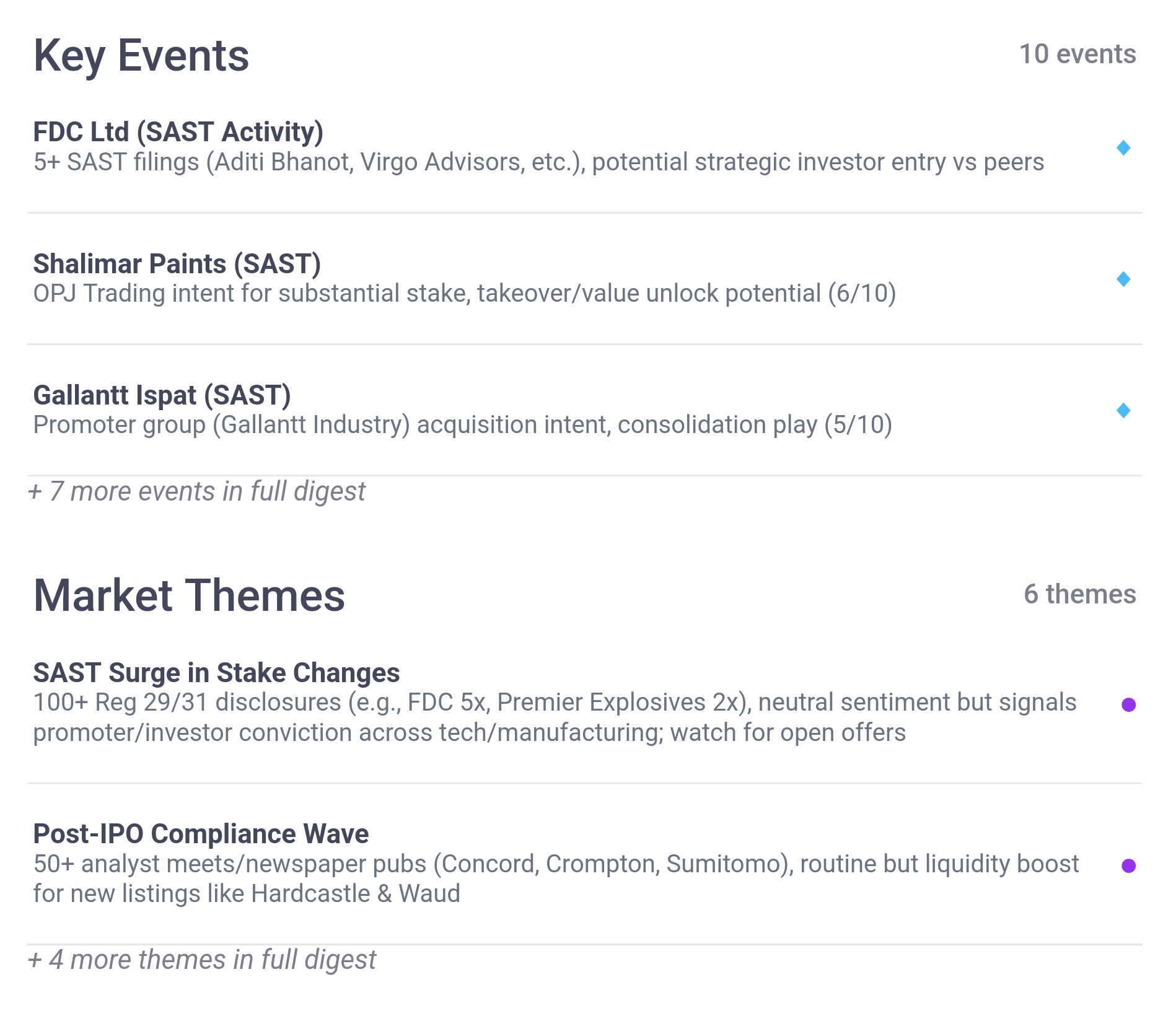

Narmada Macplast EGM

April 3 for cap hike ₹22 Cr, ₹250 Cr investments, agri pivot; e-voting March 31-April 2

◆

Nyssa Corp Postal Ballot

E-voting March 11-April 9 for dir appointments, results by April 11

◆

Responsive Industries

E-voting March 13-April 11 for Ind. Dir to 2031

◆

+ 5 more events in full digest

Promoter Confidence in Small-Caps

6 buys (e.g., Vibhor +0.03%, Anupam +4.88%) vs 1 sell (Rama -0.18%), avg +0.5-5% stakes, signals undervaluation amid NSE/BSE listings

●

Governance Stability

10+ filings w/ 98-100% approvals for dir re-appointments (Hester 99.54%, Laxmi 99.93%), low turnout but promoter 100%, reduces execution risk

●

NBFC Regulatory Clarity

4 RBI amendments (owned funds, Tier1 incl. Q profits -0.25*D*t adj., concentration norms), immediate effect aids 100s NBFCs compliance/capital planning [NEUTRAL-POSITIVE]

●

+ 3 more themes in full digest

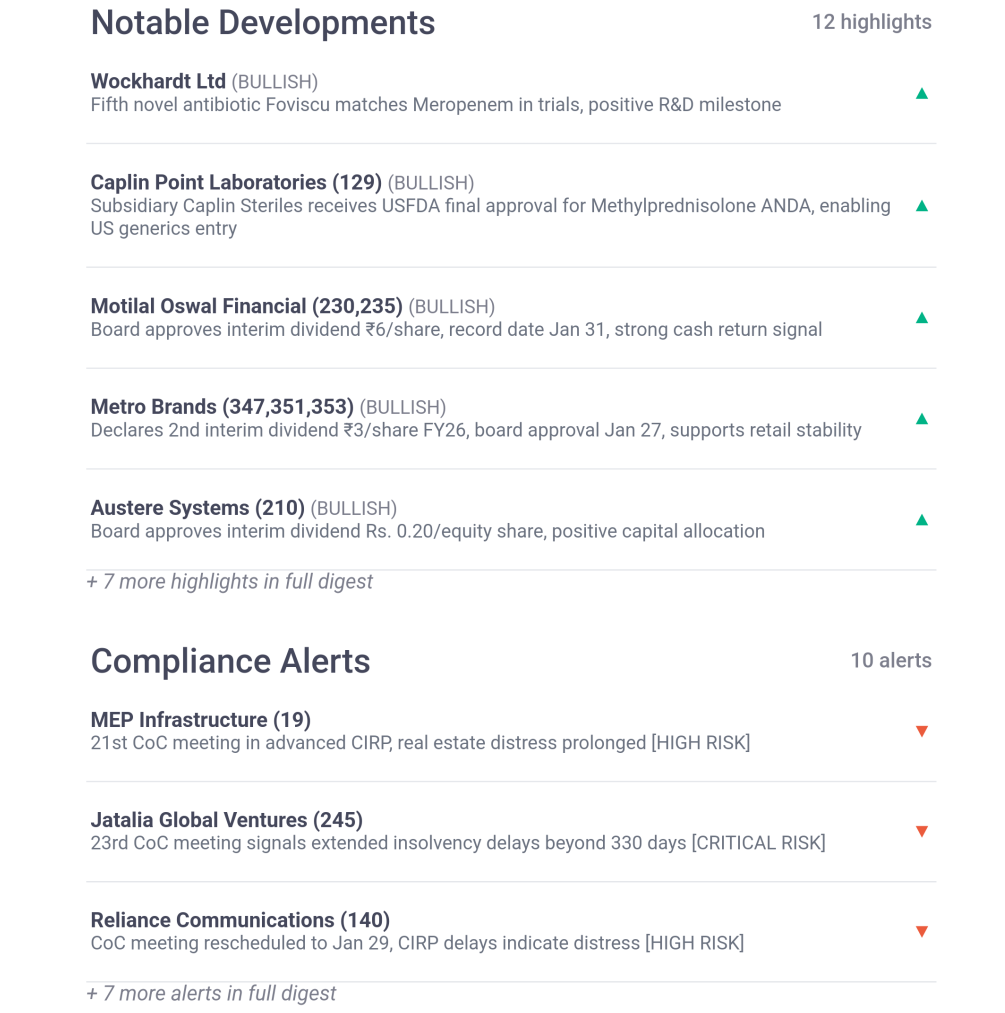

Notable Developments

12 highlights

Shalibhadra Finance(BULLISH)

Promoter group Ayushi Doshi bought 2,000 shares (holding +0.01% to 1.73%), signaling confidence despite negligible size

▲

Vibhor Steel Tubes(BULLISH)

Promoter Vijay Kumar Kaushik acquired 6,000 shares (0.03%, holding +0.03% to 21.16%) via open market at ₹110.96, modest buy indicates conviction

▲

Justo Realfintech(BULLISH)

Promoter Puspamitra Das bought 4,000 shares (0.02%, holding +0.02% to 39.49%) open market, reinforcing control

▲

+ 9 more highlights in full digest

Compliance Alerts

10 alerts

Rama Steel Tubes(HIGH RISK)

Promoter group TARUN DHIR sold 30L shares (0.18% drop to 4.77%), potential conviction loss

▼

Afcons Infrastructure(MEDIUM RISK)

Promoter encumbrance disclosure under SAST Reg 31(1), signals liquidity pressure

▼

Setubandhan Infrastructure(HIGH RISK)

FY25 net loss ₹1.51 Cr (turnover ₹23L, exp ₹1.74 Cr), CIRP delays, audit qualifications on assets/liabs (net worth ₹45 Cr vs liabs ₹170 Cr), NCLT rejection

▼

+ 7 more alerts in full digest

📂 View Complete Digest

View all 50 filings with complete AI analysis.

View Full Digest →